MediaAlpha helps insurance companies acquire internet based leads. This is currently a struggling business due to auto insurers waiting for rate increases before returning to advertising to attract new customers, which is a cyclical issue. Insurance industry advertising spending should catch up to the broader digital advertising share of marketing budgets, which should translate into sustained long term earnings growth. A major shareholder’s recent moves reflects an informed view of the company and a likely inflection point in the cycle while the secular growth opportunity remains.

On several factors (low float, debt, out of favor industry), this is a neglected stock and it appears likely that some or all of these factors could reverse in the next 12-36 months. If all goes well, it potentially trades for a 15% and still growing FCF yield in the next 2-3 years. If the company only recovers to its prior 2021 peak, it trades at 17x earnings, which probably translates into ~30% downside if it trades at an 8% yield. The potential downside where earnings are permanently stuck at the current low level seems unlikely given the auto rate hikes under way, White Mountains has re-endorsed the prospects for the company, and its largest customer is reporting high rates of growth again.

Investment Setup

1. MAX’s business is a derivative of the digital marketing budgets of auto insurers, and increasingly health insurance companies, as customers shift to online purchases. MAX operates the exchange that connects buyers and sellers of leads, which can be selected across dozens of insurance specific variables. These leads are very valuable because they are data rich and very timely, which is in contrast to generic leads. Financial apps (CreditKarma, Nerdwallet, Mint), insurance supermarkets (The Zebra, Insurify) and carriers (Progressive, State Farm, etc) collect detailed information that can be segmented very granularly. This allows for precise targeting of customers right when they have indicated a high purchasing intent.

The joke in marketing is that half the budget is wasted but it isn’t clear which half, whereas MediaAlpha addresses much of the problem that this joke highlights. Lead gen, largely driven by search engine optimization and buying keywords, is a fraught business where most of the economics go to Google, scale players are favored, and a wide net must be cast. MAX exists off of the exhaust this activity generates, because not every generator of a lead has the most profitable use for it. Ironically, this exhaust generates some of the more valuable leads that can attract multiple purchasers.

Insurance companies can purchase these leads as well as sell them through MediaAlpha. Maybe an insurance company attracts their target demographic in every way except the State they are looking to purchase insurance. Some companies may have a better handle on repair costs for Tesla vehicles and price those policies better. Companies may inadvertently acquire them and want to sell that lead on to someone who intentionally targets that profile. This partially recoups spending that can be further reinvested in additional leads (MAX claims ~30% of the cost can be recouped). This isn’t the case with a Google ad – if you pay for clicks and only want standard auto customers and nonstandard auto customers show up then you effectively wasted money, have no way to recoup it, and never really had a chance to avoid it. MAX addresses the problem in healthcare as well, with about $300m of revenue from that vertical (mostly Medicare Advantage - ~50% penetration amongst eligible users and also a low portion of ad spend on digital).

Insurers are slow movers but are increasingly shifting their focus to DTC capabilities and digital advertising. Digital ad spending in the insurance sector is 22% vs 66% for all ad spending (this is according to a MAX presentation that quotes William Blair, which isn’t really gospel but it is generally fair to portray a massive gulf in insurance ad budgets versus other industries). There is ~$10.5bn of spend that has the potential to double over the longer term and at a minimum should represent an ongoing tailwind – if it takes ~10 more years to reach 44%, that’s a 7-10%/yr revenue boost with further room to grow. MAX did $1bn of ad spend transactions in 2021, implying ~9% share.

MAX is very focused on “performance” ad spend. While Progressive is the industry leader in digital advertising, other players are increasingly forced to adapt to where customers are shopping, such as State Farm and Allstate. My understanding is that GEICO is not very active in the space, which represents a lot of upside as their spend could be comparable in size to Progressive’s.

One theory is that the fixed base of advertising spend – TV, radio, generic SEO, etc – is largely set and that all incremental dollars should flow to categories resembling the MAX solution. If MAX type “performance” spending is half of the ~20% of ad budgets spent on digital ads, it could represent close to 100% of the incremental dollars. Digital spend reaching ~50% of insurance ad budgets could 4x the TAM for MAX, and they will arguably capture a larger share of incremental dollars (10%>40%). These numbers are illustrative of how the broader market shift can have a multiplicative impact on MAX’s revenue, as an increase in MAX’s share of its target market will further boost revenue. This is perhaps overly optimistic as a large portion of digital spend growth in any category will be captured by Google, but overall this a very favorable tailwind. In theory – and possibly practice – as insurance companies spend more on leads coming through Google ads, they will have an even greater incentive to resell unwanted leads through MAX.

2. The downturn in MAX’s business is cyclically driven by poor underwriting results and a lag in regulatory approval for pricing increases in the auto insurance industry. These factors are likely to prove temporary – if not over the next 12 months then over the next 12-36 months, as there is little systemic value in unsustainable insurance companies. Car insurance rates are up 17% in the first half of 2023. Used car prices starting to fall may also offer some relief as well, although there is still pressure on repair costs.

If insurance company profits revert to the mean, this will drive a renewed focus on acquiring new customers, which will increase demand for attractive leads. This should also coincide with customers price shopping in response to higher rates, which will also increase the supply of high intent leads. This makes it likely that the snap back in business will be quite rapid and possibly visible as soon as this current quarter (Q3) or next. A newer variable that may be introduced in this auto cycle is that home insurance premiums are also registering huge increases, which will likely trigger shopping by customers who bundle auto and home. Bundled customers have higher lifetime values, which means that insurers should be willing to increase their customer acquisition costs.

Progressive releases monthly financial data and shows direct auto policies up 16% and 15% YoY in July and August, respectively. While they don’t provide granular data on the net premiums written, they are overall up 21% and 16%, respectively. This implies satisfactory pricing on policies that should drive advertising spend as insurers seek to compete more for new business. Progressive is a major MediaAlpha customer and overall spender in the digital ad space.

Allstate, another large customer (they purchased Esurance, but have since folded it into Allstate direct), has put through rate increases in most states and is in the process of pushing for approvals in a few remaining unprofitable states – they have gotten a 19% increase in rates since the start of 2022 through Q2 2023 overall, but only 9% in CA, NY, and NJ, which are 45% of their underwriting losses (page 7).

My basic impression is the MAX product works and its relevance has not been diminished in the same way its lead gen peers have struggled. It was growing rapidly through 2021 until the insurance cycle turned. The insurance cycle is less faddish than a lot of the tech IPOs that have occurred in the last few years. While insurers had a COVID windfall, demand didn’t sky rocket like it did for pools, RV’s, or boats. I don’t believe MAX has grown by giving away its product at a highly subsidized cost hoping to eventually gain some magical scale where 30% operating margins were only a few keyboard clicks in a powerpoint away like BNPL or delivery companies.

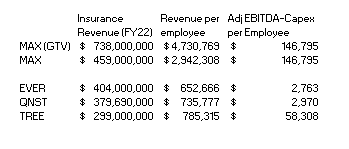

On a GAAP revenue basis, MAX generates slightly more revenue than the insurance/financial services segments of QNST, TREE, and EVER. On a gross transaction value basis, MAX was 2-3x larger at the 2021 peak and still maintains a large lead. While MAX has seen revenue drop relatively more in 2022 and 2023, their adjusted EBITDA less capex (not my ideal metric, but able to compare) has held up better, with the exception of TREE. This points towards MAX not being a stock market funded customer giveaway. This also points to the most upside if/when the cycle turns as even in 2022 they convert revenue into cash. It’s also worth noting that everyone else is structurally in a scale based competition against direct insurance companies, with far greater SEO and SEM budgets, that makes them unlikely to economically attractive over long periods of time.

3. White Mountains, a credible insurance sector investor, was an early investor in MAX. They sold shares in the IPO at $19 and more shares at $46. They recently purchased 5.9 million shares at $10 a share, in addition to already owning 17m, which is a large portion of the 7.2m shares they had sold in the last 2 years. The shares are now at $8.

It is worth paying attention when WTM write a $60m check that can be replicated in public markets at 25% less. Their purchase also dramatically diminishes probability that the late 2020 IPO was merely dumping a business on the precipice of obsolescence. While it was an opportune moment to sell down, the subsequent downturn in the business has to do with the auto insurance cycle and not being a structurally uneconomic sham. The continued growth of the health insurance vertical since 2020 is further indication a competitive threat hasn’t emerged in their niche and that their marketplace isn’t solely dependent on some quirk in the auto insurance space that is on the cusp of disappearing.

White Mountains found MAX through their investment in Esurance, who was MAX’s earliest major customer, and itself the early player in the direct digital insurance space. White Mountains has traded MAX shares very well to date. Their position in having an industry, customer, and ongoing operational understanding of the company gives their behavior very valuable informational content. I also believe there is insight into timing that indicates an informed player believes the auto insurance advertising market is highly likely to rebound in the near term, which is supported by other aforementioned data points as well. In Q3 2023, management also shifted their salary to be 90% in RSU’s, which is a cash saving measure but also a comment on their opinion of relative value.

4. White Mountains, Insignia, and 3 co-founders own a significant number of shares. White Mountains’ recent tender decreased the float further. A low float deters investors from digging into the company due to low liquidity and the likelihood of increased supply in the future from financial investors selling down their stake. This is a technical dynamic of the stock, but I think is worth noting as it contributes to the magnitude of the cheapness and then will potentially play some role in the rate and magnitude of the share price potentially increasing on good news flow. This is not a reason to make an investment, but I think it plays a big enough role to warrant highlighting and understanding.

Risks

1. I get what the company does, but that doesn’t mean I understand where it will be in the future. The base rate of success of niche advertising platforms does not really support the idea that this will exist and be going from strength to strength 10 years down the line. Google could decide to create a standardized auto insurance quote form, similar to flights or hotels, and more aggressively target the ad dollars that MAX currently captures. There could be regulation or other plumbing changes that alters MAX’s ability to collect the data that underlies its marketplace (MAX has flagged ~$1.3m of costs in 2023 for legal fees tied to an FTC investigation – there is little insight into this, but WTM increased their stake knowing about this). The MAX marketplace may also have gamification beneath the surface where the reselling of leads “bribes” larger players but slowly burns small players who eventually realize what is happening (absence of evidence, but that is not evidence of absence). Some of the recent success leading up to its recent peak in 2021 may have been driven by the emergence of players like Root and Lemonade that spent a lot of money to acquire customers and are now fading into obscurity. There may have also been an above trend jump in digital ad spend as people were staying at home during COVID. This may have had an impact on both volume and price of leads in the MAX exchange, although this likely misses the huge shift to digital ad spend by the entire industry, which was already underway before COVID and appears to still be ongoing.

While MAX is not directly a Google SEO algorithm, some of its customers are essentially that. One has to believe that SEO is a cost of doing business that should endure even if individual businesses trying to game it are ultimately fads. It is possible this marketplace is sufficiently niche that Google doesn’t pay attention, but that also contradicts the massive growth opportunity MAX claims. MAX claims deep data integrations with insurance companies, but at the end of the day there are few employees and little capex, which are the two conceivable barriers to data integrations or honing algorithms. The irony is that at the point they seem to have achieved huge success – like $5bn in GTV – will be when they attract the most attention and it will only be voodoo gibberish to convince you they will hold their ground and keep thriving.

2. The TAM may be a bikini statistic. As one example, agent based insurance models aren’t going away and may be a reason that digital marketing spending in the insurance vertical is lower than the broader digital marketing wallet share. A portion of car insurance is bundled with home insurance. A large portion of health insurance is handled by employers. I also suspect a large portion of insurance ad spending will always be focused on brand recognition campaigns that are basically everything except what MAX is focused on. MAX has a nascent agent focused initiative under way which may yield fruit, but it remains to be seen how aggressively they will spend on digital marketing. While this still leaves a lot of room for MAX to play, it may also mean the business hits a wall sooner than expected. The company is expanding in health and life insurance, which is logical, leverages costs, and helps diversify revenue but may also be a sign that the auto facing part of the business is really only capable of getting so big.

The second point worth noting about the TAM is that MAX’s is focused on a very specific slice of it. Changes that have an existential impact may be hard to discern from the outside until it is too late. This is the most volatile portion of ad spend, which means MAX has a volatile business. Perhaps this makes it less attractive to new entrants and weeds out the weaker existing competitors, but all things considered this is a harder business in the scheme of things. All sorts of problems can emerge in a volatile business, which can lead to suboptimal decisions, which can lead to suboptimal outcomes.

3. There is debt and the business is currently at break even levels. The covenants seem quite relaxed – e.g. they get to adjust out $10m of public company expenses – which gives breathing room. The company does not require much in the way of capex or capitalized intangibles either, so adjusted EBITDA is able to service the debt. There are also tangible guideposts – media reports and Progressive’s monthly releases- that imply advertising revenue could be on the verge of inflecting higher, which will further mitigate this risk.

4. The valuation I’m about to pencil out is very much forward looking. This is not a low multiple stock. There is a wide dispersion of potential outcomes. While MAX is a play on the auto insurance rate cycle, its specific exposure to direct carrier marketing spend may behave in unforeseen ways that make it less correlated to the underlying improvement in the auto rate cycle.

The valuation in part hinges on large stock based compensation not being recurring. The cofounders all got a large RSU grant at IPO and have been sellers at higher prices. They may view future grants as necessary to “reload” their alignment. I suspect WTM and Insignia viewed the grant as a cost of doing business to get the shares listed while the market was hot, but will not be as generous in the next plan. While in general I would not assume this about a company, the specific circumstances mitigate the potential for a large ongoing SBC add back in adjusted EBITDA.

Valuation

There are 46.2m Class A shares and 18.1 Class B shares, which convert on a 1:1 basis, and another 5.2m of restricted shares, so there are 69.5m shares outstanding. At $8 each that is a market capitalization of $556m. There is $170m of debt. Enterprise value is $726m.

Lets take a stab at valuation relative to normalized earnings. The company did $58m of EBITDA on $1bn of gross transactions in 2021. Interest expense is about $15m/yr, there is no capex or capitalized intangibles, and I assume a tax rate of 25%. I use GTV because 2/3 of revenue comes from a marketplace with gross revenue recorded and 1/3 from fee based transactions where net revenue is recorded. Even without the sexy secular growth angle, $58m of EBITDA in the near term on a rebound would still put the company close to 17x $32m of net income, which isn’t high relative to the growth potential.

The attractiveness of the investment is predicated on the continued secular growth and cyclical rebound in digital advertising by insurance companies combined with the evidence that this is already a workable product. If the medium term secular growth rate is in the 25%ish range, normalized GTV should be $2bn by 2025, if based off the 2021 results. The broader demographic forces that drive the shift to online spending continue every year even if the insurance cycle doesn’t drive those results in a given year (this is the crux of the WTM thesis). The company is not profitable right now, but has been in the past. The main driver – auto rates – is visible and rate increases are underway, so this differs from almost all VC promotes that went public in recent years.

If the company has earns 7% EBITDA margins on the increase from $1bn to $2bn in GTV, that puts that company at $128m of EBITDA, which should be about $85m of net income. That implies a ~10% EBITDA margin on GAAP revenue, which they achieved 2019-21. If this takes 5 years to happen and there is still some line of sight on another doubling of GTV, I suspect this will trade at more than 6.5x earnings.

While this is just playing with numbers, the company’s broader trajectory over the last 5 years, ongoing auto rate increases, and White Mountains’ behavior point towards reasons for optimism. Without getting into a specific multiple, as the company increases the size of its health insurance business and expands into other verticals, the volatility of the auto insurance business should only dampen rather than collapse profitability.

While not crucial at these prices, out year GTV beyond $2bn will make the current valuation seem puny. More fantasies include White Mountains playing a critical role in further savvy capital allocation that gives the impression of a higher probability of a blue sky future being delivered in a shareholder friendly manner. There is also the potential that someone views this as an attractive asset to acquire and WTM helps ensure that a healthy premium emerges from a competitive auction (Lending Tree purchased Quote Wizard for 23x adj EBITDA and 4x revenue).

Conclusion

MediaAlpha is an interesting business with some interesting signals around WTM’s tender offer, Progressive’s monthly results, and the overall increase in auto insurance rates under way. While not cheap on current earnings, a cyclical inflection combined with a continued secular shift appears underway that could result in the valuation being low.