Maaku Renaado マーク レナードChronicles

Guiding Thoughts on Japanese Software Companies

Japan’s Abenomics started when it made the most sense for Japan. Digital transformation (DX) is following a similar path. Demographic, economic, and government pressures make it likely that Japan speed runs 20 years of IT investment in the next 5 years and continues to grow nicely from there. This process was autocatalyzed due to the 2020 shock of Covid forcing the Japanese to fully confront the need for DX. It was already fully articulated by METI in 2018 and a known long running economic vulnerability. Japan presents companies with a unique competitive ecology that limits the number of suppliers that simultaneously faces an existentially driven demand wave. There are numerous companies with low valuations and even lower nominal size that are set to ride this capital light high margin wave of software in Japan that have a probability of emerging as category leaders.

Opportunity

Call me Maaku Renaado マーク レナード the way I’m about to shill software from a capital allocation perspective (that’s “Mark Leonard” put in a Japanese name converter). The core bet is that we are still early and valuations don’t reflect it. IT spending remains low in Japan relative to other countries and the penetration of cloud spending as a percent of IT budgets lags dramatically - ~18% in US, 12% in Europe, and ~4% in Japan (this stat may be ~2 years old, which is a long time given high growth rates, but the US has continued to grow cloud spend double digits over this period). The explosive growth seen during the pandemic has moderated, but the long term trend still points to double digit growth for a long period of time.

The Japanese people are wealthy and not stupid. There are 124 million of them. Even with a declining population, Japan will remain a large addressable market with the economic structure, budget, infrastructure, and digital literacy in place to upgrade its software stack.

The necessity of increased investment in and adoption of cloud based software is on the new side of a punctuated equilibrium post-covid. This contrasts to the American experience which has experienced SaaS and cloud computing as a steady evolution over the last 25 years. Most importantly the Japanese themselves recognize this out of self-interest across all levels of society - individual, SME, corporate, and government – as both a financial and existential issue.

Japan did not suddenly identify the need for Digital Transformation (DX), but the present moment sees DX already underway compared even to 2019. The government is proactively pushing more digitalization. Since 2018, METI has been discussing the 2025 Digital Cliff, their name for the rapid falloff in the ability to maintain legacy on premise complex black box customized software, 60% of which are now over 20 years old. About 80% of IT budgets go towards maintaining existing systems, many of which are increasingly outdated. The cost of maintaining outdated systems was pegged at JPY 12trn, about $80bn/yr, which is ~2% of GDP. This exerts a massive cost on the Japanese economy, which creates abundant opportunity for overhauling its digital infrastructure. The budget for IT investment already exists but is being poorly allocated into an increasingly inefficient burden.

An important subtext to black box systems that are difficult to maintain is that increasing geopolitical tensions and cybersecurity risks make them a major vulnerability. This risk can be partially mitigated through the cloud (e.g. on prem system could be totally bricked without off site redundancies, older systems are the most likely to have easily exploited vulnerabilities). This is a further incentive for the government to take seriously and prioritize DX, as these concerns likely become more pressing over time. National security risks give DX initiatives salience to more conservative leaders that may otherwise have no particular interest in giving their support.

METI is walking the walk. For example, 500-1,000 employees are using a project management software, Backlog (1.4m users in Japan), to reduce paperwork and time spent keeping track of tasks. This is a good example of the white paper writers no longer just writing white papers. METI also has a dedicated website to promoting DX at SMEs, as well as another dedicated website walking SMEs through the various subsidies available to them, including an IT implementation subsidy.

At a more granular level, at the start of 2024, only 10% of companies were considered “DX-promoting” by the IPA, which is Japan’s Information-technology Promotion Agency (table created in March 2024 – can read for more). While likely not all encompassing, it is directionally supportive of the idea that the post pandemic growth is very far from over. While this may not have the heft of the Tokyo Stock Exchange Name & Shame on capital allocation, it is a good proxy for how underinvested Japanese companies are. METI also collaborates with the IPA and TSE to highlight noteworthy and platinum DX companies, so the IPA rankings tie into social incentives in capital markets.

“Analysis”

There is a strong element of a supply and demand imbalance in Japanese software that has some very attractive capital cycle dynamics. This is favorable for investment opportunities in a way that electric vehicles or AI lack. Many software companies can achieve power law outcomes and face little competition. The risk/reward is very attractive given these circumstances.

Supply

There are not enough software engineers to build products, case studies to demonstrate their efficacy to customers requiring a lot of up front information for vetting, and few international suppliers prioritizing localization of their software and business cultures. This should favor the first companies to solidify their presence in the market with a credible product since SaaS adoption is happening on a compressed timeline. Time is a physical fabric of the universe bottleneck. Bottlenecks in tech talent and tech savvy workforces reciprocally amplify the tension in the time bottleneck.

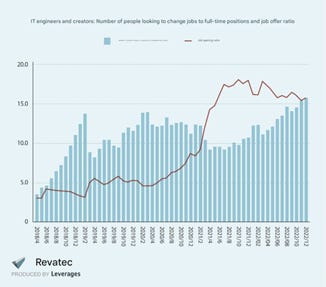

Competitors would have to develop a comparable offering at the same time as the adoption curve is compressed, but with what surplus technical talent and bottomless entrepreneurial risk taking appetite? There are 15 times as many IT engineer job openings as there are people looking to change jobs and this gap is 3x larger than when METI first warned of the 2025 Digital Cliff in 2018, a function of increased demand and a shrinking workforce.

The VC ecosystem and start up culture is much smaller in absolute and relative terms (report on VC in Japan and Internationally and post on the state of VC in Japan for the curious). It also seems that foreign VC is not a major player at the earlier stages – both because there are existing Japanese sources of capital and foreign players have more limited value to add to an investee besides cash if they have not operated in the market for a long time. This further constrains the supply of new entrants relative to the US. This positions already established companies with modern solutions to capture the majority of growth going forward. This will be more pronounced in niche markets or those with increasing returns to scale, which is often an inherent factor of many software applications.

In a country with a consensus oriented business culture and where the nail that stands up gets hammered down, I expect there to be far more consolidation around the existing players who sell cloud software. In one example, there are 5 approved government cloud providers for public agencies in Japan, including Microsoft and Google, but as of October 2024 1,452 out of 1,497 systems are using Amazon Web Services. I do not believe this will be an exception given the positive flywheel that a SaaS business model can unlock.

Vendor consolidation is reciprocal to supply constraints in IT labor markets. Japanese companies do not have large IT departments. Purchasing decisions often defer to the actions of the industry leaders who may have larger IT departments, such that companies who sell to the leaders have already done most of the heavy lifting and need to manage their onboarding resources to work their way through the market. This is particularly true in Japan, which is consensus driven. Here is a CEO for a company that sells software to a highly regulated and large customer base that is underinvested in software as an industry and especially underinvested in this specific application being sold:

In fact, when we tell our customers that "other companies do it this way," we show them a list of our customers. Then, they respond by saying, "If Company A and Company B are using it, we'd like to hear more about it."

So we set up a meeting between the three companies, and they explain, "This department and that department have never communicated with each other before, but this is how we communicate.

Then, they will say, "Oh, so that's how it's done," and once they understand the practice, they will be able to visualize it and make a purchase. We focus on getting existing customers to support us during the sales process.

When many best practices emerge, when customers get together, they discuss things like, "How will you respond to this request?", "We use their product, and this is how we do it now," and "So we use their product after all." This can lead to increased sales speed.

In order to shorten the lead time, if you focus on improving the product for existing customers, you can create success stories. Once you have a success story, that company can tell other customers, and they will say, "So that's how you set up the operations," and the lead time will be shortened.

Rather than increasing our in-house staff, we believe that the more we can increase customer satisfaction at our existing business partners and become the de facto standard among industry companies, the less resources we will need.

Separately, here is a story about how one the largest used auto retailers is implementing DX. They have a $750m market cap. The key point is that they are creating an entirely different subsidiary, which will have different pay scales and work rules. This company stands out as being very proactive in addressing their IT needs, but it also highlights how most companies are not well staffed with IT talent.

IDOM plans to "promote in-house system development" (President Hatori) and will also strengthen its recruitment of IT talent. In May 2024, it established a DX subsidiary, IDOM Digital Drive, to recruit IT engineers, and began full-scale operations in September of the same year.

What is unique about IDOM Digital Drive is that employees hired are immediately seconded to the parent company, IDOM, and work in IDOM's IT department. This is clearly different from the "subcontractor position" often seen in Japanese system subsidiaries. In recent years, this type of structure has been called a "receptacle-type system subsidiary."

IDOM has not disclosed the salary levels at the new company, but systems subsidiaries that serve as a base for recruiting generally offer salaries higher than those of the parent company to make it easier to recruit IT engineers, and most also offer remote work and flexible working arrangements.

In fact, IDOM Digital Drive's job postings include annual salaries of over 10 million yen. "Nearly 90% of the employees who were originally working in IDOM's IT department have already been transferred to the new company," said President Hatori. IDOM Digital Drive has not yet decided on its hiring plans.

IDOM has embarked on a large-scale investment, invited a reform leader from outside, and established a new company to steer the company toward digital transformation. However, the shortage of IT engineers in Japan remains serious. The key to the company's success in digital transformation seems to be how well it can provide an attractive environment for IT engineers and gather talented colleagues.

An alternative delivery mechanism for software is through Systems Integrators (SIers), which do in effect control a lot of IT departments to the point of being the de facto IT department. SIer solutions often lack the agility of dedicated SaaS providers and are competitively disadvantaged as time goes on, as they have more constrained addressable markets. Corporations are generally aligned with specific SIers, majors such as NTT Data, TIS, SCSK, Fujitsu, such that the concept of a best of breed solution proliferating out of an SIer faces the obstacle of divergent incentives (certain SIers have industry specialties such as Fujitsu in hospital EHR software). SIers want to drive customers towards solutions that may be more beneficial to the supplier than the customer. They often get paid on a per person per hour basis, which further highlights divergent incentives. Corporate IT departments are often referred to as “order takers,” as in other departments ask for features or changes, which are then relayed to SIers to actually implement. This is not conducive to innovation or best practice implementation. SIers will continue to exist and pose some competitive threat to pure play SaaS companies but are mostly notable for soaking up IT talent to create structurally worse products in a way that limits competitive supply being broadly available.

Demand

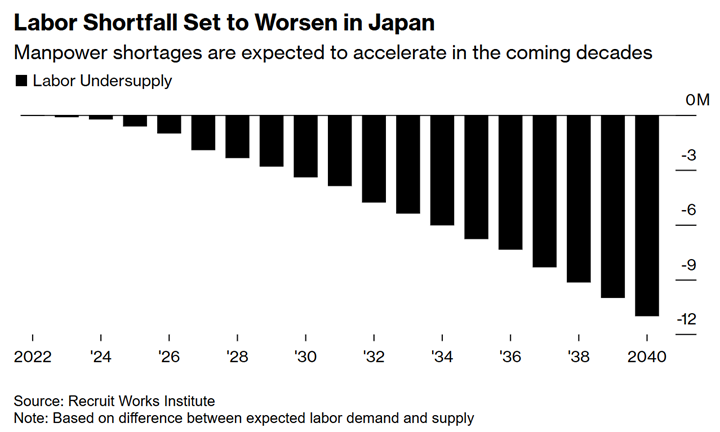

What is happening on the demand side of Japan’s tech infrastructure is at the point of existential, far beyond the concerns of the 2025 Digital Cliff. There aren’t enough people to perform the existing jobs in the economy, so Japan will have to improve productivity if it is to maintain its standard of living. SaaS often replaces paper and excel based workflows that are time consuming. This can help address productivity issues very broadly. There has been the “2024 Problem” where labor laws initiated more oversight on overtime, further reducing aggregate workhours, further incentivizing productivity enhancements. The 2024 Problem is in more manual labor such as construction or logistics, but it is emblematic of broader demographic forces pushing for a rethink of processes.

There are also more general IT labor constraints as seen in other countries, such as with COBOL engineers retiring, that encourage a shift to software systems that can be more easily maintained. More unique to Japan is that some IT staff are closer to being one-of-one when it comes to understanding the customized systems built up over decades.

There is a broad endeavor by the Japanese government to introduce legal requirements that foster adoption of digital systems, which adds systemic pressure for additional digital uptake. For example, My Number Card, brings every Japanese person into a digitally legible system that will ease access to a variety of government programs, which will also have to be managed in a digitally legible way. This is occurring in invoicing and social insurance coverage, where modern digital systems are required to comply with the laws. These visibly force adoption of software, but beneath the surface they also highlight further the pain point of continuing to adapt dead end on premise customized solutions. This should act as a procyclical force that encourages further adoption of software solutions when thinking about how the market will evolve over the next 5-10 years.

An underappreciated aspect of self interest in DX driving demand is at the microeconomic level. It is a massive improvement in job quality right as the market for employees is becoming even tighter. The existence of much more efficient and better staffed companies is an economic threat to businesses that are inefficient and poorly staffed. This was not an intense dynamic in earlier stages of SaaS in the US, as the concept was still being proven and the competing products in 2012 were mostly not traditional paper processes or software products custom designed in 1992 (for an American equivalent 2025 Digital Cliff, 60% being 20 years or older), and unemployment was higher.

There is more power in the hands of employees due to the number of job openings in Japan, which strongly suggests that the companies that have the least burdensome processes are in a better position to attract or retain revenue generating employees, as well as pay competitive salaries. The rate of midcareer job transitions is increasing from a low level in Japan, which should further encourage companies to update their processes to have the fewest unnecessary burdens that discourages their staff. This is doubly true for IT professionals, who have very in demand skills and typically receive low pay at traditional companies. The movement of talent out of these roles to more efficient and modern software players further exacerbates the difficulty of maintaining internally developed customized black boxes. Some examples of these forces at play:

Today, however, talented younger workers are far more willing to take a chance on a new firm than their parents were. Four decades ago, 70 to 80 percent of people in their late 20s or early 30s who had worked for one employer for ten to 15 years stayed at that employer for at least another ten to 15 years. By the early 2000s, that rate had dropped to 50 to 65 percent, and now statistics indicate that less than half of young workers stay at the same firm for so long. The shift is also apparent in the hiring of people in the middle of their careers. Back in 1994, only 35 percent of companies hired anyone in their 30s and 40s away from another firm; now, 70 percent do so, and those that do are more profitable as a result. In the lifetime employment system, workers tended to develop company‑specific skills. Given today’s rapidly changing and uncertain conditions, firms benefit from incorporating new skill sets and perspectives through hiring midcareer workers.

A virtuous cycle has begun. Workers have greater leverage in the current tight labor market, and now, with established firms more willing to make midcareer hires, they feel emboldened to take risks. Newer companies have been able to recruit both veterans from more established firms and recent college graduates. Take the recruitment firm Visional, founded in 2009, which matches companies, new and old, with potential candidates. By 2023, it had found jobs at 20,000 companies for 2.3 million well-paid employees seeking better opportunities, and in 2021, its founder became Japan’s newest billionaire. Visional is now just one of many such recruitment agencies.

Newer firms have also been able to take advantage of a pervasive problem in employment practices among traditional firms: the lack of equal pay and promotion opportunities for women. I recently spoke to two female executives at Askul, a distributor of office supplies. They had left household-name companies to join Askul in its early days (it now has sales in the billions of dollars), lured not only by better opportunities for advancement but also by the adventure of building something from the ground up. The newer companies do not yet have sufficient weight to reduce the national gender gap in pay and promotion, but the more talented women they recruit, the more pressure traditional firms will feel to close the divide.

Technological advances are also increasing the market power of startups. In the past, new firms had difficulty reaching customers because they had to use a distribution system for products that was largely controlled by big legacy companies. E-commerce has changed that. Take Rakuten, Japan’s flagship Internet mall. In 2023, some 57,000 small and medium enterprises sold more than $40 billion worth of products to over 100 million customers through the site, which functions much like Amazon. One of Rakuten’s merchants is Tansu No Gen, a former furniture maker and now a seller whose founder was wary of e-commerce and preferred using traditional retail stores. When he retired in 2002, his children joined Rakuten’s network, and they saw sales explode from less than $1 million per year in 2002 to $175 million today.

Digitization is putting enormous pressure on Japan’s more staid companies to look in new directions. In a ranking done by IMD Business School of 64 countries in “digital agility”—how much a company increases sales and profits for every dollar it invests in digital equipment and software—Japan came in dead last. That struggle to master digitization is one of the reasons Japanese giants have had trouble competing in world markets. As a result, some traditional companies now feel compelled to work with digitally adept newcomers. In 2018, for the first time, the number of software vendors exceeded traditional parts makers among the top 5,000 suppliers to the automaker Toyota. Few of the software companies wanted to join Toyota’s corporate group and be treated as subordinates rather than partners. They cherished their independence, including the freedom to collaborate with anyone, even Toyota’s competitors. Toyota’s need for outside technological expertise for all the sophisticated electronic software and hardware in vehicles these days forced it to abandon its long-standing reluctance to allow its vendors to work with the competition. In order to innovate, it has accepted conditions that it had previously disdained.

Is there money to be made?

Many of the opportunities I find most compelling are tiny companies with controlling shareholders – 40-70% floats on $10-200m companies aren’t inviting a lot of scrutiny from individual or institutional investors. The Japanese microcap retail investor is one of the least fundamentally driven in the world. Some other factors include Japanese markets not being interested in EV/ARR valuations, even if the company has 70%+ gross margins, no SBC, huge white space, and very compelling LTV/CAC ratios. Mature margins aren’t just a promise 2-5 years out at this point. Companies with intermittent and low profitability are also not eligible for Prime listings on the Tokyo Stock Exchange, which further dampens interest in the short term.

The growth rates for a lot of software companies in 2020 and 2021 were very high, but from a low base – 50%+ YoY. Price charts show a company IPOing, entering a down 75-90% freefall as growth rates and hyperinterest couldn’t be sustained, and then remaining relatively flat for the last 2-3 years. Revenue multiples for the broader SaaS industry in Japan have collapsed from 20x to ~5-6x, with many companies trading below 2x revenue despite signs of continued growth and profitability. This is psychologically discouraging, but unlike SPACs from this era, these are real companies that went public during a buoyant time.

Growth rates still range from 15-30% for many companies. This should continue for much longer than current valuations seem to anticipate given the lagging adoption of cloud-based IT catching up to a still ongoing increase in cloud software in the US and Europe. Much in the way that 5 or even 10x revenue was cheap in hindsight for US SaaS in the early 2010’s, Japanese SaaS at low revenue multiples is similarly cheap given the clear opportunities ahead. While not all are “cheap” in the backwards looking sense, it is cheap relative to the economics they can generate as growth continues (e.g. 20% operating margins on doubling revenue takes a co from 3x revenue to 1.5x revenue and 7.5x EBIT with continued high margin growth opportunities). Another compelling feature for more traditional investors is that Japanese companies have a broader cultural imperative to be profitable that has a double benefit of being easier to wrap one’s head around a DCF while making a money losing competitor rushing to catch up a lot less feasible. Even a medium term holding period likely won’t entail tolerating the paradoxical nature of running at breakeven to secure the market longer term.

Venture Capital

A distinction with VC money in Japan is that companies are going public at much earlier stages, not after a Series Q round where VC horse trading mark ups capture all the upside of the rapid part of the growth curve. Japanese corporate venture capital (CVC) and VC seem to sell down their stakes in the IPO and then after a 180-360 day lock up. This isn’t novel, but it is worth pointing out that they are doing so into a heavily retail oriented buyer base, as there are few institutional Japanese microcap players.

CVC is typically small checks relative to the size of the investor and mainly meant to improve their own products. Salesforce is a major CVC player in Japan to encourage companies to build their products on Salesforce, with direct profits on the investment a secondary or tertiary consideration. These are also very smalls sums to Salesforce. This should also act as validation of the opportunity for software overall in Japan, as Salesforce is far more active in Japanese CVC than most other countries.

There are also CVC players like JR East, the railway, looking to spur innovation that may help better monetize their real estate footprint. Even Japan Post has a VC arm. These aren’t forced sellers, but they are not seeking to maximize investment profits directly through ownership of these stakes. I sense that CVC money is preferable to overseas Silicon Valley VC money, because the corporation is bringing specific and local business opportunities that are mutually beneficial. All of this is to say that many of the sellers of shares in younger tech companies are receiving economic value primarily through the activities of their core business rather than proceeds from investments.

The incentive to go public early is higher in Japan since there are prestige and recruiting benefits from being publicly listed. The media-centric hype cycle seems relatively absent in Japan, although I simply might not have found the spaces where such narratives are promoted. This means that there is not a cheerleading VC PR campaign building up excitement over several years prior to an IPO or successive funding rounds to achieve a higher mark in their fund.

Corporate Governance

There are still corporate governance reforms yet to be done. Most young tech companies have not announced a shareholder return policy yet. This leads to a lack of interest that could contribute to lower valuations, although this is a backwards looking viewpoint. Outright hostility seems like less of a possibility post Abenomics. The reality is that young companies growing rapidly shouldn’t be returning cash to shareholders quite yet. A cash rich balance sheet is an asset in a company’s growth because it gives customers, who are far more conservative in their purchasing decisions in Japan, more confidence in the longevity of the company.

In one encouraging example, Plus Alpha Consulting, an enterprise HR software company, announced a 5% buyback at the end of 2024 as the share price had fallen dramatically, while the company is still growing ~20% with ~30% operating margins (currently ~4x/18x forward revenue and net income). They announced this on November 29th, 2024 and were already 20% through it by January 10th, 2025. This is in line with country wide increases in buybacks and dividends in recent years, but confirms that tech companies are not oblivious to capital market trends.

More broadly, many tech companies have detailed presentations, sometimes in English, even at <$20m market caps. This could be seen as an indication of management desire to attract investors, which increases the odds they don’t have an insular mentality and will ultimately adopt reasonable payouts at the appropriate time. It also helps that there are share grants outstanding at many of these companies. If employees stand to exercise options equal to 6-10% of the company, there is probably greater internal pressure to also do what is necessary to maximize the value of those.

Risk

Competition

The major risk is either fast follower SaaS startups outflank some of the early leaders or that on premise software providers make the shift to a SaaS business model. Given less sprawl of SaaS applications, it may make sense for the ecosystem to take advantage of the blank slate and build on top of more established players, as can be seen with companies built atop Google Workspaces or Salesforce. This may have implications I do not fully grasp. These are general risks that are mitigated by the understaffed nature of the Japanese IT ecosystem, the smaller size of the Japanese VC community, and the relatively lower appetite for entrepreneurial ventures in Japan.

While the on premise to cloud business model transition for individual software companies is also a well-trodden path in the US, the starting valuation for the Japanese SaaS players is a lot lower. While this is an ongoing risk worth monitoring, the hints of legacy players adeptly responding with their own cloud offerings have yet to emerge. OBIC may be an exception to this and is a formidable domestic ERP provider, but they do not satisfy every software need in the economy. If I understand the SIer ecosystem, there are not many nationally dominant providers to displace, as much of the existing software are more customized systems.

In a specific example, a legacy on premise software provider I researched does have monthly pricing plans and a cloud service, which offers a lower entry price and some off site backup. The monthly pricing plan is for on premise style software that is still more expensive than the SaaS competitor. The cloud service is an additional cost and is just hosting the on premise software elsewhere for customers, not a program simultaneously updated across all customers. This type of company will typically require customers to submit requests for any changes to the software. This could be as simple as moving a field in form or adding a new field. This has the facile resemblance to SaaS, but does not offer any of the benefits for customers of a SaaS solution. It is also structurally higher cost – e.g. you need an engineer making requested changes rather than having a systems architecture that allows the customer to customize immediately without intervention.

Culture

The Japanese are Japanese. Japan already had the lowest productivity among major developed countries prior to the pandemic. There may be factors illegible to the outside world that constrain software adoption beyond the bare minimum, since Japan has been unswayed by lagging productivity in the past. Many employees may still harbor a fondness for a paper heavy way of doing business, especially older ones. DX may just end up making paper forms into digital forms, with only minor changes that don’t sustain a wave of software adoption, such as data analytics applications. It’s not as if every corner of the German or Italian economy has embraced every single digital capability possible, so expectations should be tempered on the speed or inevitability.

Like the early stages of Abenomics, the cultural reason to be doubtful is very legible in the rear view mirror, but there is now Japanese self-interest and economic necessity that should spur change on Japanese terms, not on the basis on top down economic theory. Japanese business culture focuses on longevity. The existential reasons to increase digital adoption are far more convincing as appeals to self-interest rather than copying US levels of IT for the sake of catching up to the same output in a data table put together by comparative economists. While the pace may undershoot high expectations, the risk that it doesn’t occur seems to be receding and requires less speculation today than a highly optimistic DX thesis given in 2019 given how much the pandemic catalyzed adoption. Japanese culture is also capable of moving quickly once a consensus has been reached, which make Italy or Germany less direct comparisons.

Technology

Japan may leapfrog a lot of the assumptions of the current paradigm due to advancements in artificial intelligence or other unforeseen innovation. The barrier to creating software may fall rapidly to the point where the supply bottleneck Japan faces turns into an incentive to speed up the adoption of faster ways to write code. While I believe this is more of a risk in horizontal rather than vertical software markets, it could mean fast followers have little difficulty catching up in terms of the modules that compose and differentiate a given software system.

This risk is offset by the present and pressing need for software. More AI-centric development processes may take a few more years to be broadly accepted. In the meantime, the emerging players currently entrenching themselves will also benefit from any efficiencies in software development combined with benefiting from existing customer relationships that will be harder to dislodge. The low valuation of many Japanese companies offers some protection from a massive derating on this eventuality approaching suddenly.

Process Oriented Thoughts

This is a cyber shoe leather affair. My preference is for companies that have clear signs of being one of, if not the, leaders in their niches. I’ve tried to do an intellectually honest Talmudic reading of a lot of Japanese material using Google Translate. There is a lot of subtext in how Japanese people communicate, although there are lots of cultural interpreters that decode communication styles (the most basic one is that a 3.5 star review is a good review). I have endeavored not to work from first principles. The more qualitative musings are pattern matching sociology utilizing observations of others with Japan experience (e.g. employer and product review scales are on the same scale as restaurant reviews, corporations are highly siloed by departments, and IT staff is usually employed by a third party). I’ve gone through marketing materials, filings, presentations, transcripts, and websites for the companies, their competitors, and broader industry players. Online reviews help triangulate the clarity of the value proposition and relative quality of the products.

How do I approach competitive analysis of Japanese software companies? The ideal Japanese software company from a customer’s perspective is publicly traded, profitable, has a clear website with numerous case studies, and is hosting regular seminars to demonstrate its product in front of potential customers (these are in person and can then get posted to YouTube and reconstituted as blog posts).

A distinct aspect of the Japanese market is a preference for lots of case studies, which helps to overcome traditional respect for existing processes. The case studies are critical to the multistep highly documented purchase process, which even has its own word in Japanese, ringisho. Case studies are referenced before a potential customer reaches out to speak to a salesperson. Companies have rigorously documented internal processes. Case studies tend to highlight the ways in which customers can replicate those processes digitally and/or with greater ease. The case studies provide social proof in a consensus driven and risk averse culture. Case studies are a strong signal that a positive flywheel is already underway and a lack of case studies is indicative of a failure to gain traction.

Default Japanese behavior is to seek reassurance a counterparty will exist over the long term. Ringisho revolves around satisfactorily answering someone in a department that won’t even use the software asking, “will this company be around in 10 years?” Public listings and profits convey staying power of a company, which is likely another obstacle for private Western companies or private startups in Japan. This concern is referenced generally, but a good example is Class Method, a $300m revenue software reseller that is private but publishes financials on its website. This is somewhat distinct to Japan and is not random. Management teams directly remark that customers want to purchase from profitable companies.

Many small companies go public for no other reason than to be public (this may also be a pitfall from an investment perspective). This is seen as a mark of credibility as a supplier and employer. I have seen software review sites where a company’s name will look like “The Magic Bakery, Ltd. (listed on the Tokyo Stock Exchange: 1234”), as well as job listings note in the header that a company is publicly traded. A company that is public and has more case studies than a private competitor is likely to be the superior player.

Conclusion

There is a compelling opportunity in Japan’s digital transformation due to favorable supply/demand dynamics for software related companies in Japan. Looking out over the long term, many current players will likely exist at much larger scale due to the likelihood that incremental entrants find a web of obstacles to traction. This overview is meant to serve as context for specific opportunities in Japan.